What Can We Do with Large Covariance Matrices?

Clustering and Regression?

Xi (Rossi) LUO

Health Science Center

School of Public Health

Dept of Biostatistics

and Data Science

ABCD Research Group

Feburary 12, 2019

Funding: NIH R01EB022911, P20GM103645, P01AA019072, P30AI042853; NSF/DMS (BD2K) 1557467

Goals

- Define a

global criterion, instead ofpair-wise "closeness" criteria, for variable clustering - Regress covariance matrix

outcomes on vectorpredictors

Slides viewable on web:

bit.ly /hacasa19

or

BigComplexData.com

Clustering

Co-Authors

Florentina Bunea

Cornell University

Christophe Giraud

Paris Sud University

Martin Royer

Paris Sud University

Nicolas Verzelen

INRA

fMRI data: blood-oxygen-level dependent (BOLD) signals from each

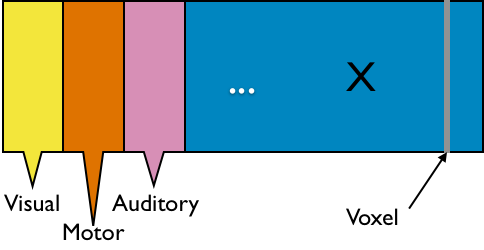

Data Matrix

- Matrix $X_{n \times p}$, all columns standardized

- $n$ time points but temporal correlation removed, like iid

- $p$ voxels but with spatial corraltion

- Interested in

big spatial networks- Voxel level: $10^6 \times 10^6$ cov matrix but limited interpretability

"Network of Networks"

- Hierarchical Covariance Model (a latent var model)

- Some ongoing research related to this model

- How to cluster variables together?

- How to estimate cluster signals?

- How to estimate between-cluster connections?

- This talk on how to

group(clustering) nodes- Usually NP-hard and limited theory

Example

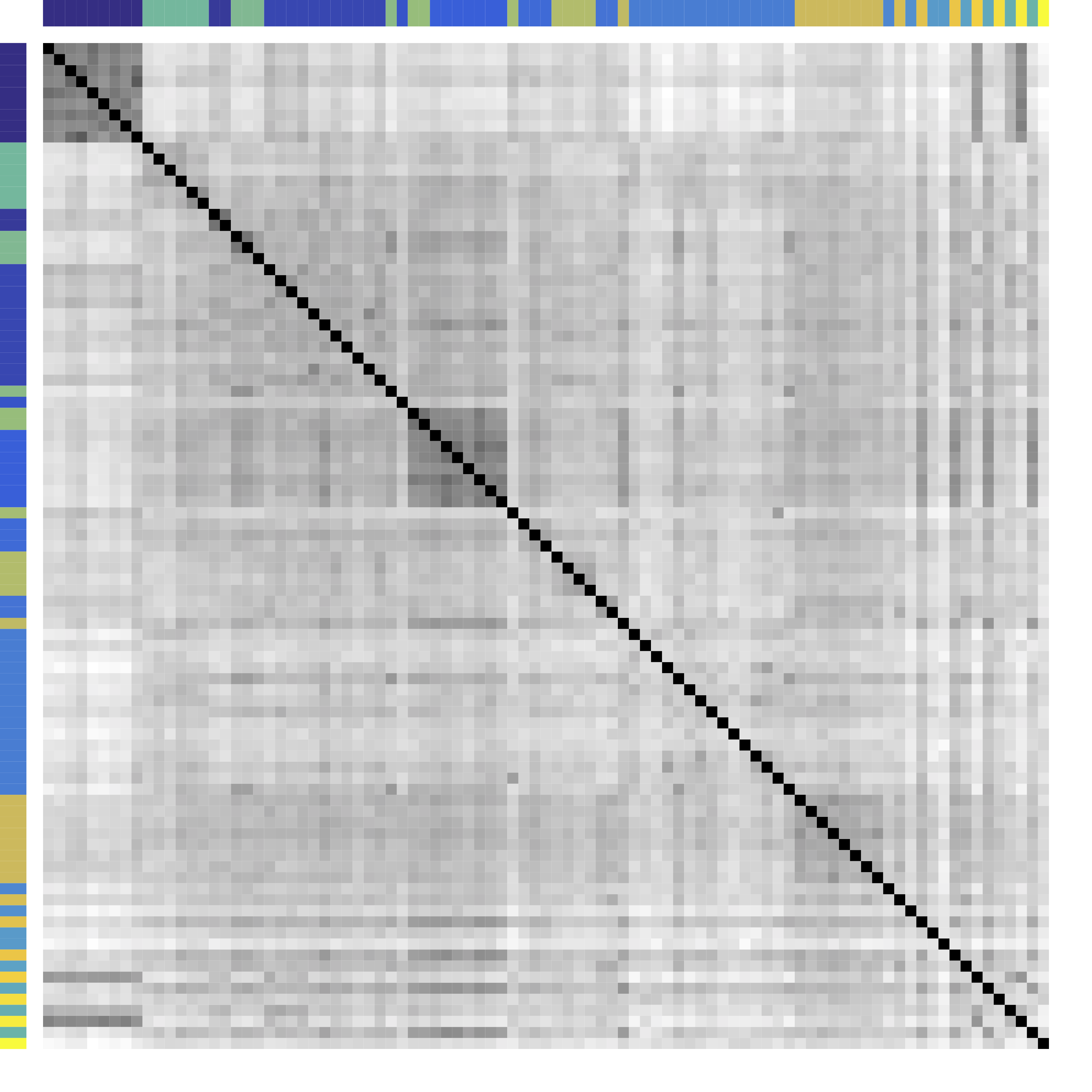

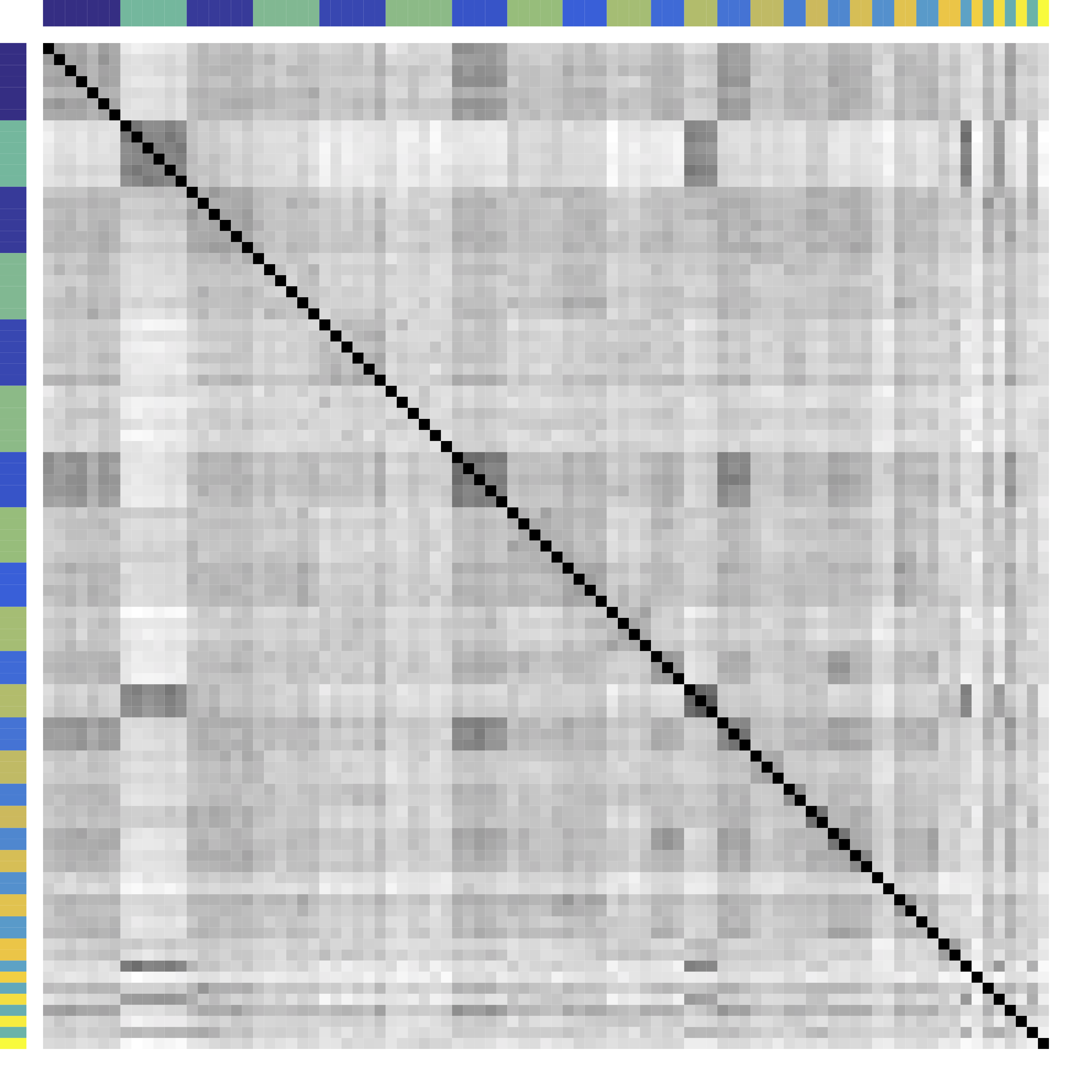

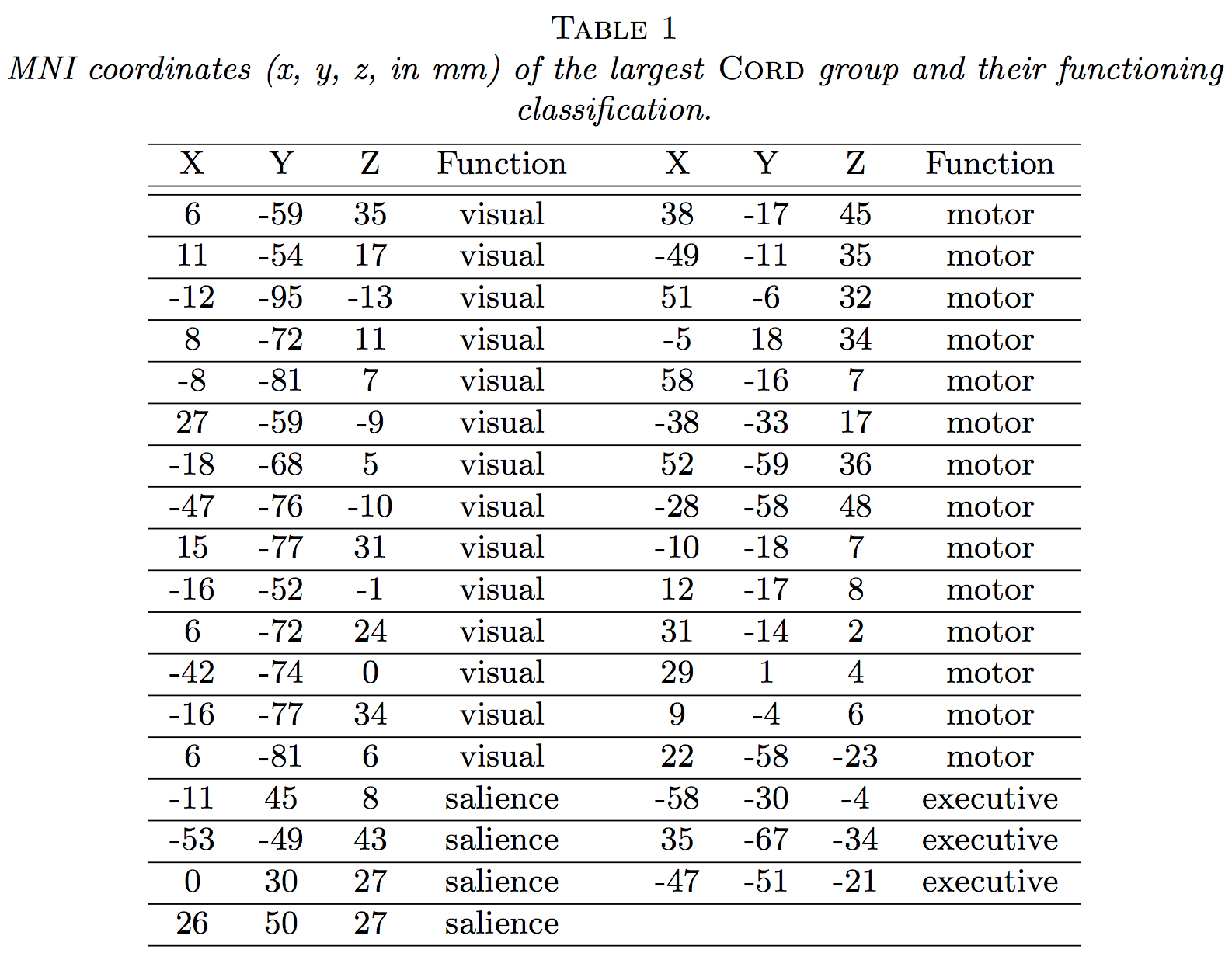

Example: SP 100 Data

- Daily returns from stocks in SP 100

- Stocks listed in Standard & Poor 100 Indexas of March 21, 2014

- between January 1, 2006 to December 31, 2008

- Each stock is a variable

- Cov/Cor matrices (Pearson's or Kendall's tau)

-

Re-order stocks by clusters - Compare cov patterns with different clustering/ordering

-

Cor after Grouping by Clusters

Ours yields stronger

Color bars: variable groups/clusters

Off-diagonal: correlations across clusters

Clustering Results

| Industry |

|

Kmeans | Hierarchical Clustering |

|---|---|---|---|

| Telecom | ATT, Verizon | ATT, Verizon, Pfizer, Merck, Lilly, Bristol-Myers | ATT, Verizon |

| Railroads | Norfolk Southern, Union Pacific | Norfolk Southern, Union Pacific | Norfolk Southern, Union Pacific, Du Pont, Dow, Monsanto |

| Home Improvement | Home Depot, Lowe’s | Home Depot, Lowe’s, Starbucks | Home Depot, Lowe’s, Starbucks, Costco, Target, Wal-Mart, FedEx, United Parcel Service |

| $\cdots$ | |||

Model

Problem

- Let ${X} \in \real^p$ be a zero mean random vector

- Divide variables into partitions/clusters

- Example: $\{ \{X_1, X_3, X_7\}, \{X_2, X_5\}, \dotsc \}$

- Theoretical: define

uniquely identifiable partition $G$ such that all $X_a$ in $G_k$ are statistically"similar" - DS: find

"helpful" partition that show cov patterns

Related Methods

- Clustering: Kmeans and hierarchical clustering

- Advantages: fast, general, popular

- Limitations: low signal-noise-ratio, theory

- Community detection: huge literature see review Newman, 2003 but start with observed

adjacency matrices

Kmeans

Low noise

High noise

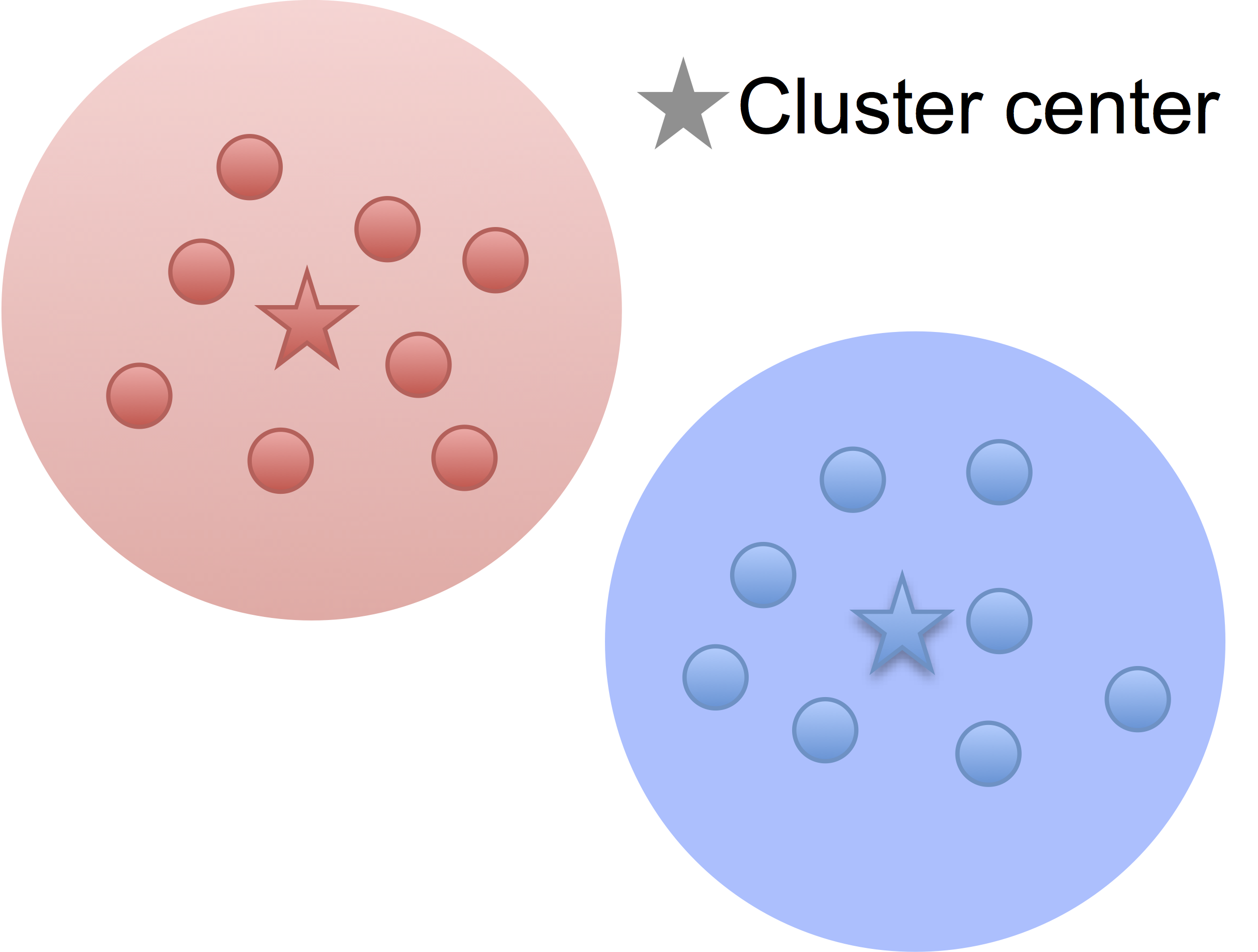

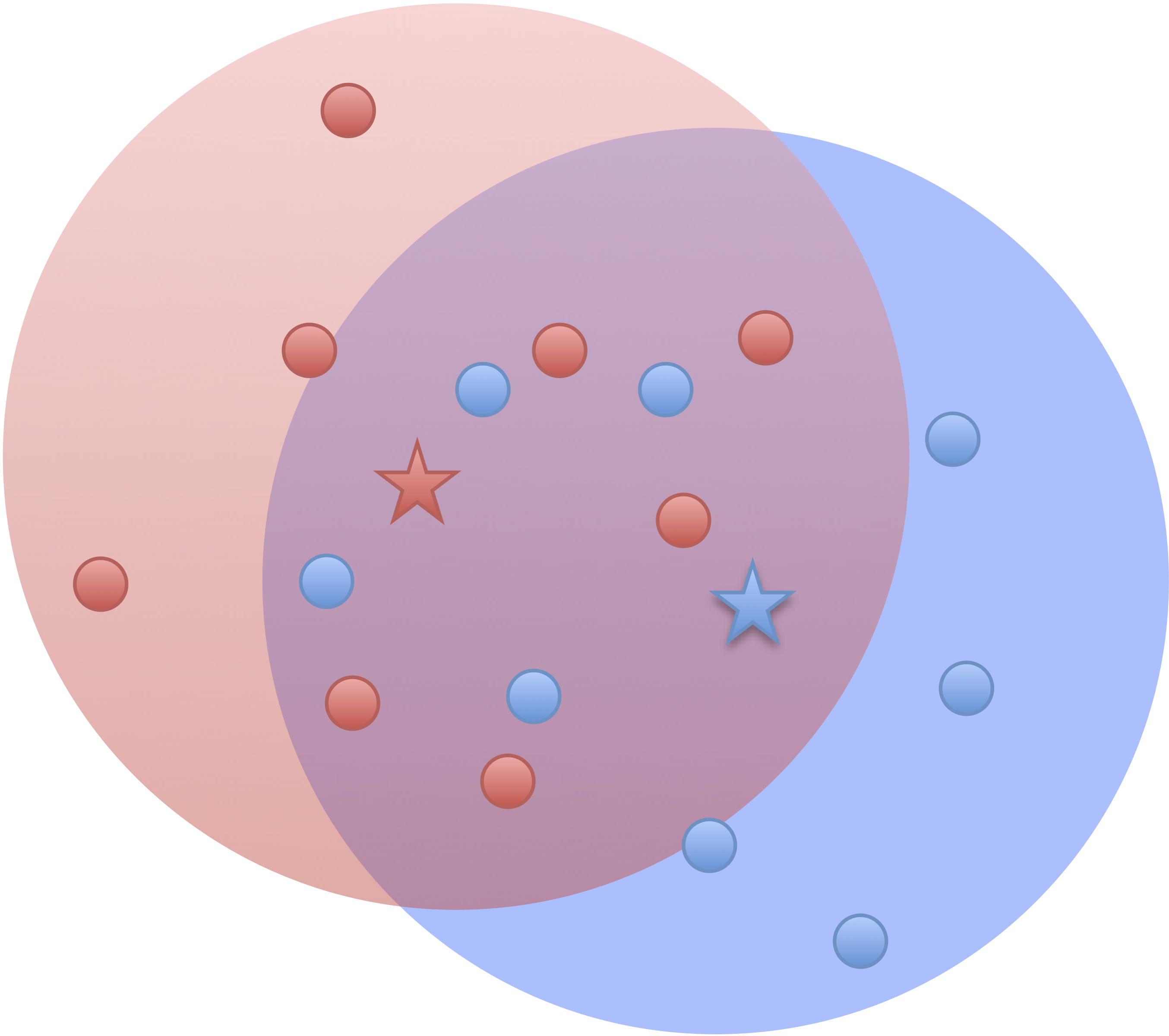

- Cluster points together if pairwise distance small

- Clustering accuracy

depends on the noise

Kmeans: Generative Model

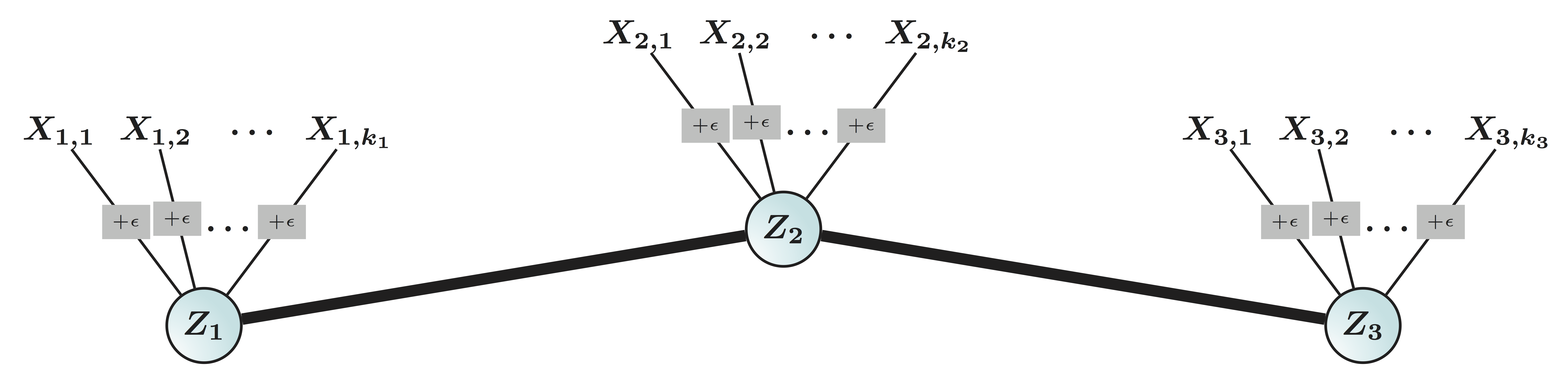

- Data $X_{n\times p}$: $p$ variables from partition $G$: $$G=\{ \{X_1, X_3, X_7\}, \{X_2, X_5\}, \dotsc \}$$

- Mixture Gaussian: if variable $X_j \in \real^n$ comes from cluster $G_k$ Hartigan, 1975 $$X_{j} = Z_k + \epsilon_j, \quad Z_k \bot \epsilon_j $$

- Kmeans minimizes over $G$ (and centroid $Z$): $$\sum_{k=1}^K \sum_{j\in G_k} \left\| X_j - Z_k \right\|_2^2 $$

$G$-Latent Cov

- We call $G$-latent model: $$X_{j} = Z_k + \epsilon_j, \quad Z_k \bot \epsilon_j \mbox{ and } j\in G_k $$

- WLOG, all variables are standardized

- Intuition: variables $j\in G_k$ form net communitiesLuo, 2014

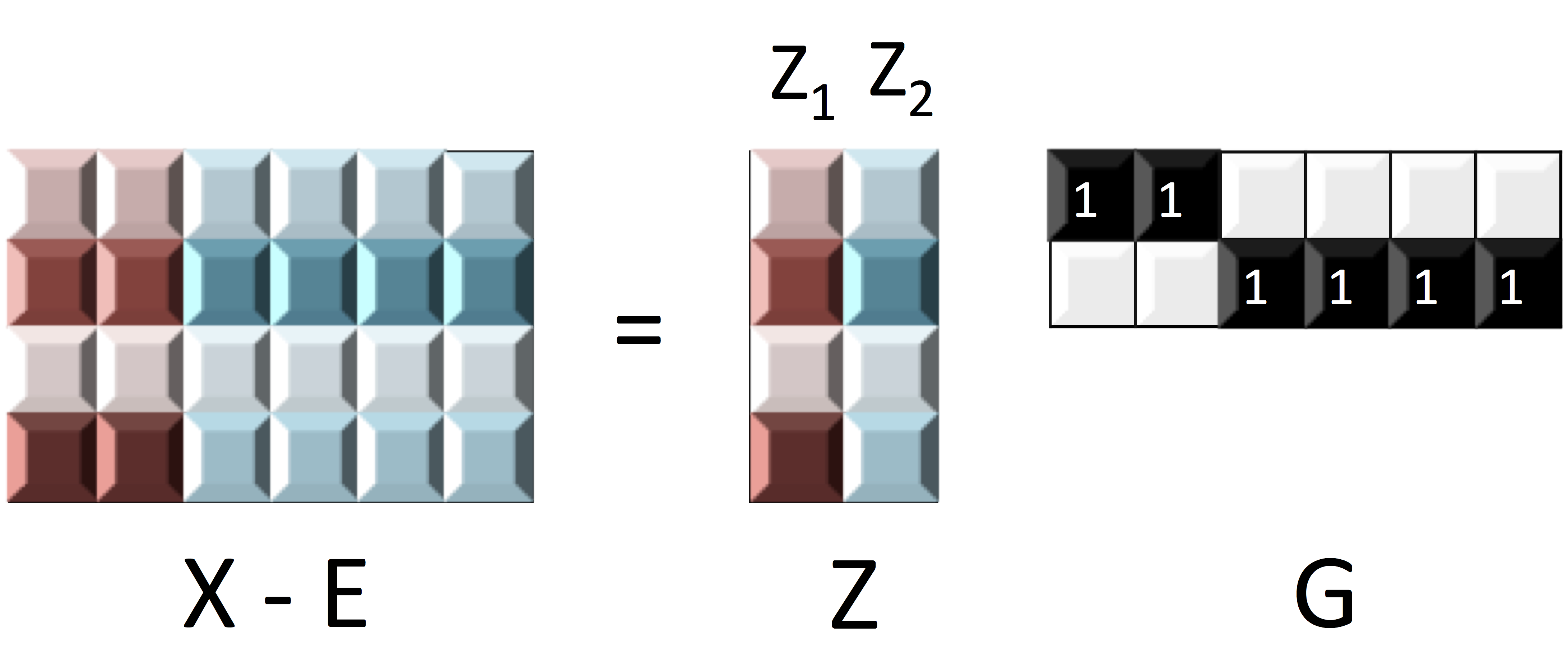

Matrix Representation

$$ X_{n\times p}=\underbrace{Z_{n\times k}}_\text{Source/Factor} \quad \underbrace{G_{k\times p}}_\text{Mixing/Loading} + \underbrace{E_{n\times p}}_{Error} \qquad Z \bot E$$

- Clustering: $G$ is $0/1$ matrix for $k$ clusters/ROIs

- Decomposition: under

conditions - PCA/factor analysis: orthogonality

- ICA: orthogonality → independence

- matrix decomposition: e.g. non-negativity

- Our model

identifiable even if $\cor(Z_1, Z_2) \ne 0$- Two brain clusters red/blue talk to each other

- Identifiable if "$\cor(Z_1, Z_2) \gt \var(Z_1)\gt \var(Z_2)$"

- Other models

identifiable usually if $\cor(Z_1, Z_2) = 0$

Principals Behind Other Clustering

- The Euclidean distance for hierarchical clustering and Kmeans, for two columns/voxles $X_a$ and $X_b$: $$ \|X_a - X_b \|_2^2 = 2(1-\cor(X_a, X_b)) $$

- Cluster $a$ and $b$ based on these

two variables only, and this isNOT what we will consider in $G$-models - Recall $X_i = Z_k + E_i$ $i \in G_k$

- Cor depends

mainly on $\var(E)$ if SNR is low - Distance

- larger even if generated by same $Z$ and large error

- smaller even if generated by different $Z$ and small error

- Worse, clusters close because of correlated $Z$

Generalization:

Latent Var $\rightarrow$ Block Cov

Example: $G$-Block

-

Set $G=\ac{\ac{1,2};\ac{3,4,5}}$, $X \in \real^p$ has $G$-block cov

$$\Sigma =\left(\begin{array}{ccccc} {\color{red} D_1} & {\color{red} C_{11} }&C_{12} & C_{12}& C_{12}\\ {\color{red} C_{11} }&{\color{red} D_1 }& C_{12} & C_{12}& C_{12} \\ C_{12} & C_{12} &{\color{green} D_{2}} & {\color{green} C_{22}}& {\color{green} C_{22}}\\ C_{12} & C_{12} &{\color{green} C_{22}} &{\color{green} D_2}&{\color{green} C_{22}}\\ C_{12} & C_{12} &{\color{green} C_{22}} &{\color{green} C_{22}}&{\color{green} D_2} \end{array}\right) $$ - Matrix math: $\Sigma = G^TCG + d$

- We allow $|C_{11} | \lt | C_{12} |$ or $C \prec 0$

- Kmeans/HC leads to block-diagonal cor matrices (permutation)

- Clustering based on $G$-Block

- Generalizing $G$-Latent which requires $C\succ 0$

Minimum $G$ Partition

Method

New Metric:

CORD

- First, pairwise correlation distance (like Kmeans)

- Gaussian copula: $$Y:=(h_1(X_1),\dotsc,h_p(X_p)) \sim N(0,R)$$

- Let $R$ be the correlation matrix

- Gaussian: Pearson's

- Gaussian copula: Kendall's tau transformed, $R_{ab} = \sin (\frac{\pi}{2}\tau_{ab})$

- Second, maximum difference of correlation distances $$\d(a,b) := \max_{c\neq a,b}|R_{ac}-R_{bc}|$$

- Third, group variables $a$, $b$ together if $\d(a,b) = 0$

The enemy of my enemy is my friend!

Image credit: http://sutherland-careers.com/

Algorithm: Main Idea

- Greedy: one cluster at a time, avoiding NP-hard

- Cluster variables together if CORD metric $$ \max_{c\neq a,b}|\hat{R}_{ac}-\hat{R}_{bc}| \lt \alpha$$ where $\alpha$ is a tuning parameter

- $\alpha$ is chosen by theory or CV

Theory

Condition

Consistency

Minimax

Choosing Number of Clusters

- Split data into 3 parts

- Use part 1 of data to estimate clusters $\hat{G}$ for each $\alpha$

- Use part 2 to compute between variable difference $$ \delta^{(2)}_{ab} = R_{ac}^{(2)} - R_{bc}^{(2)}, \quad c \ne a, b. $$

- Use part 3 to generate "CV" loss $$ \mbox{CV}(\hat{G}) = \sum_{a \lt b} \| \delta^{(3)}_{ab} - \delta^{(2)}_{ab} 1\{ a \mbox{ not clustered w/ } b \} \|^2_\infty. $$

- Pick $\alpha$ with the smallest loss above

Theory for CV

Simulations

Setup

- Generate from various $C$: block, sparse, negative

- Compare:

- Exact recovery of groups (theoretical tuning parameter)

- Cross validation (data-driven tuning parameter)

- Cord metric vs (semi)parametetric cor (regardless of tuning)

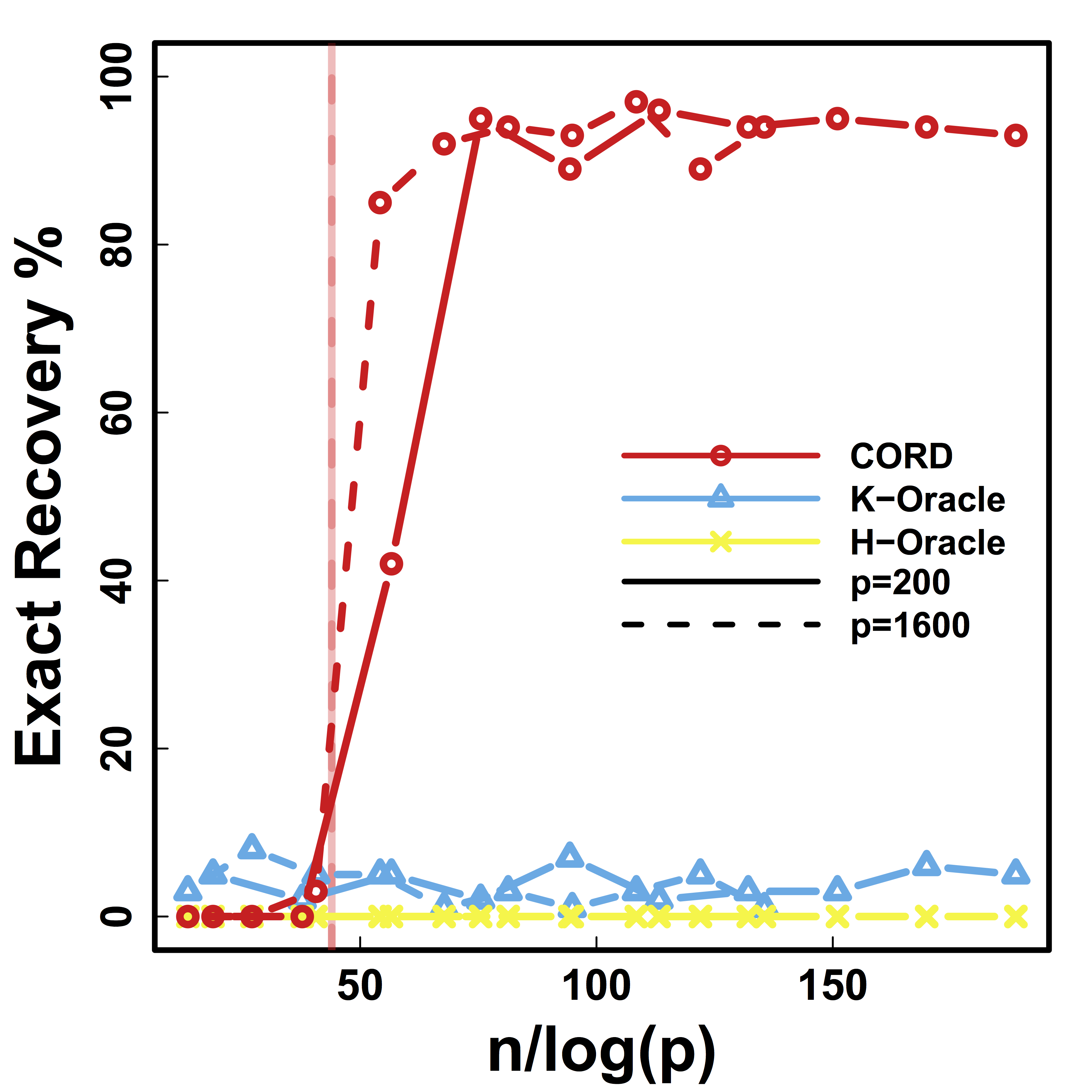

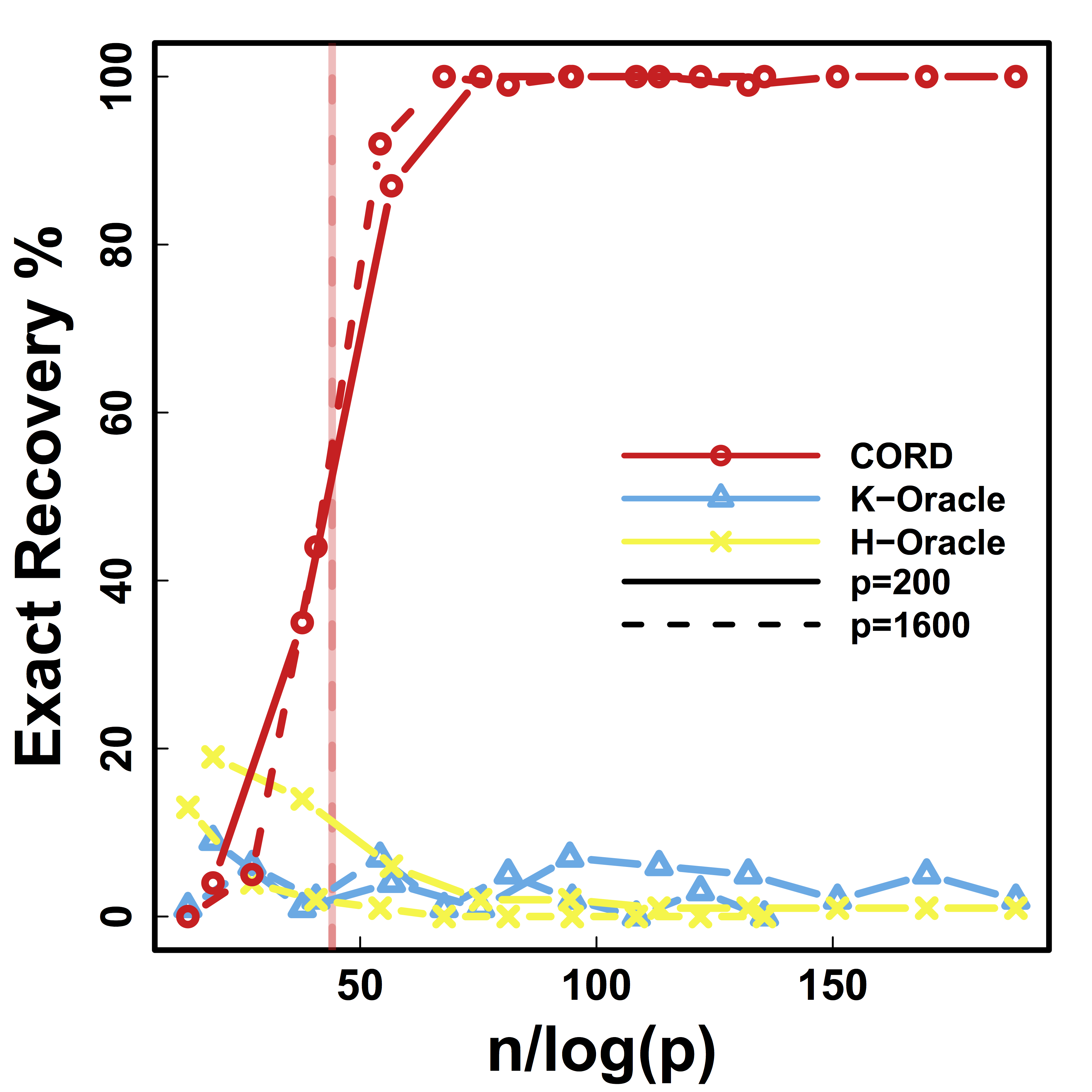

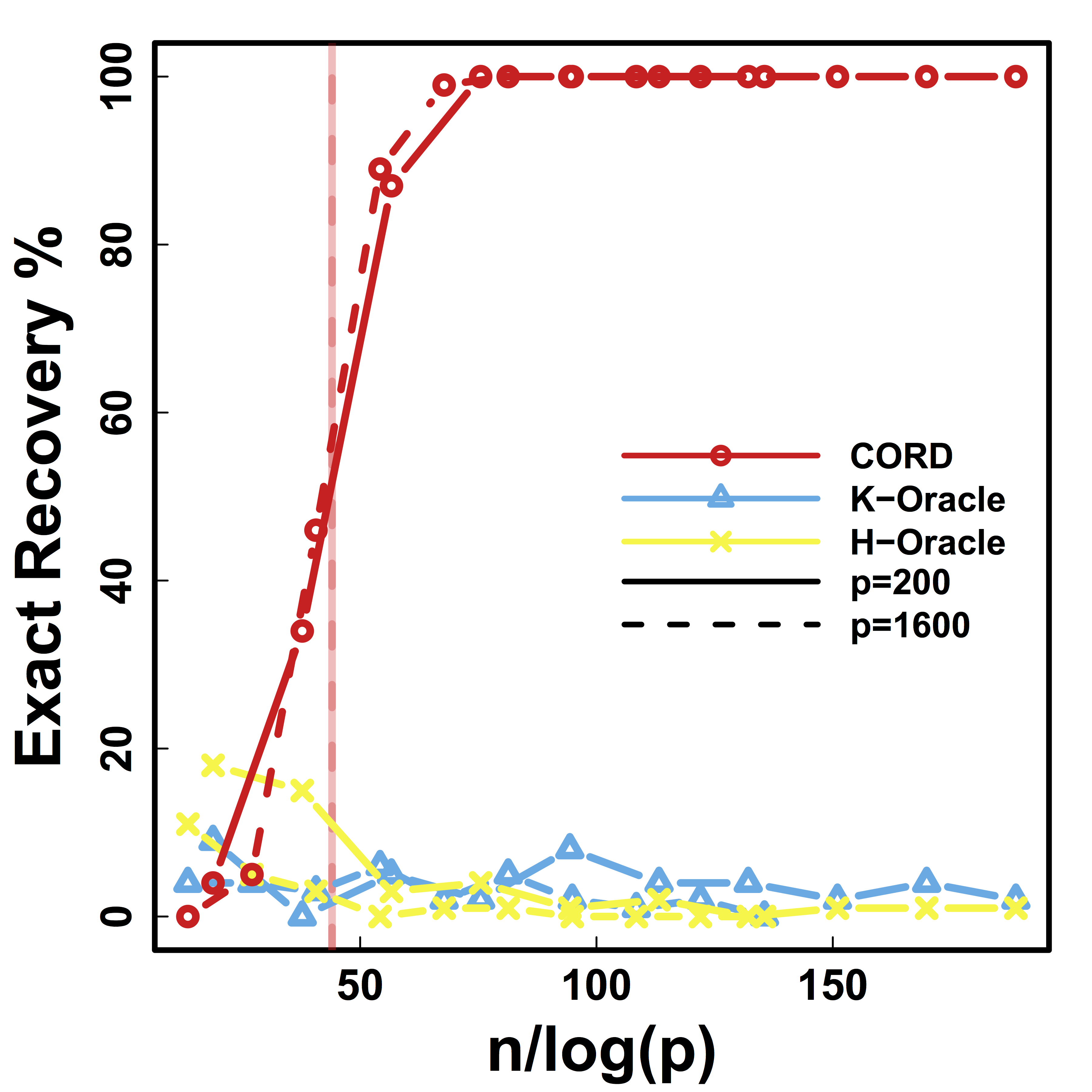

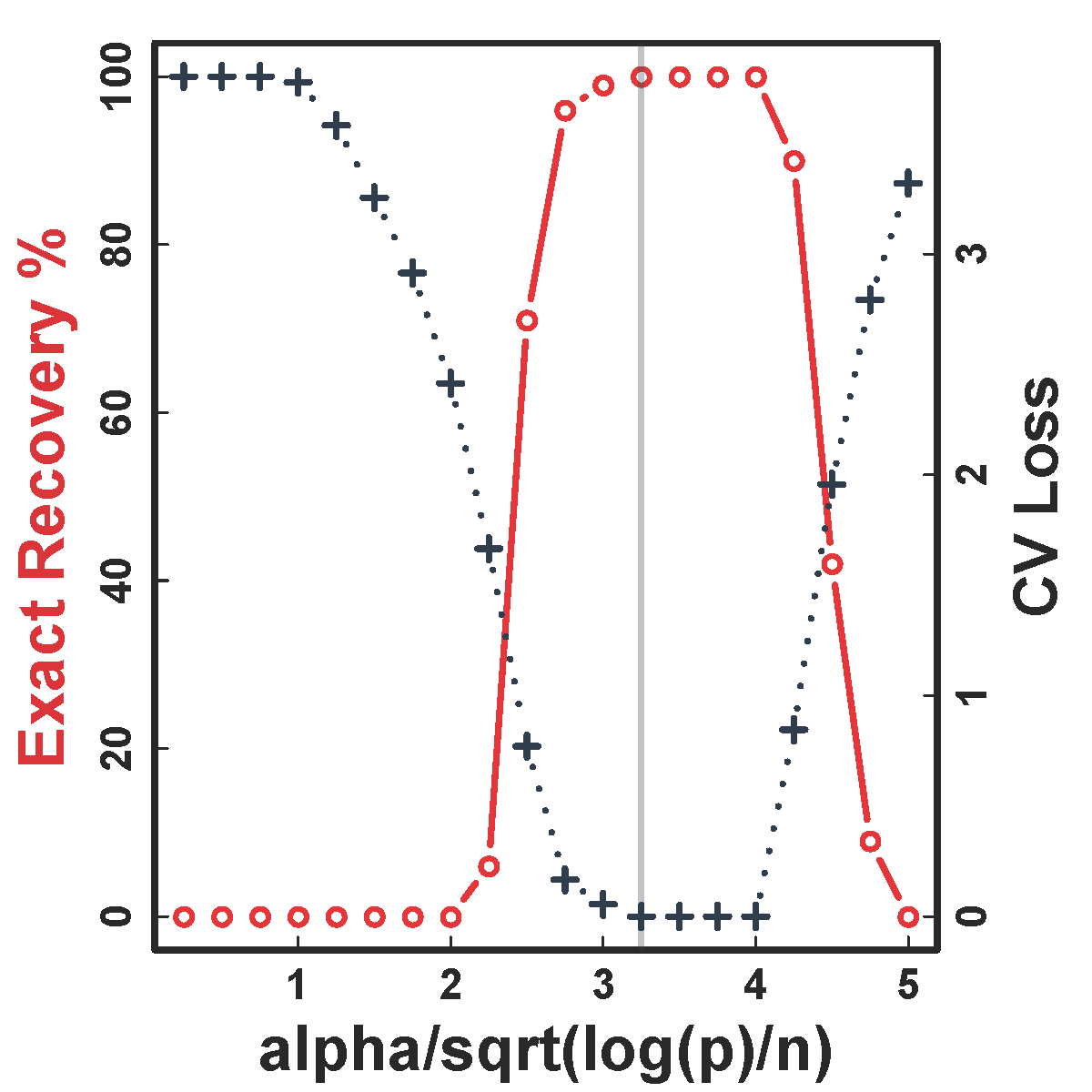

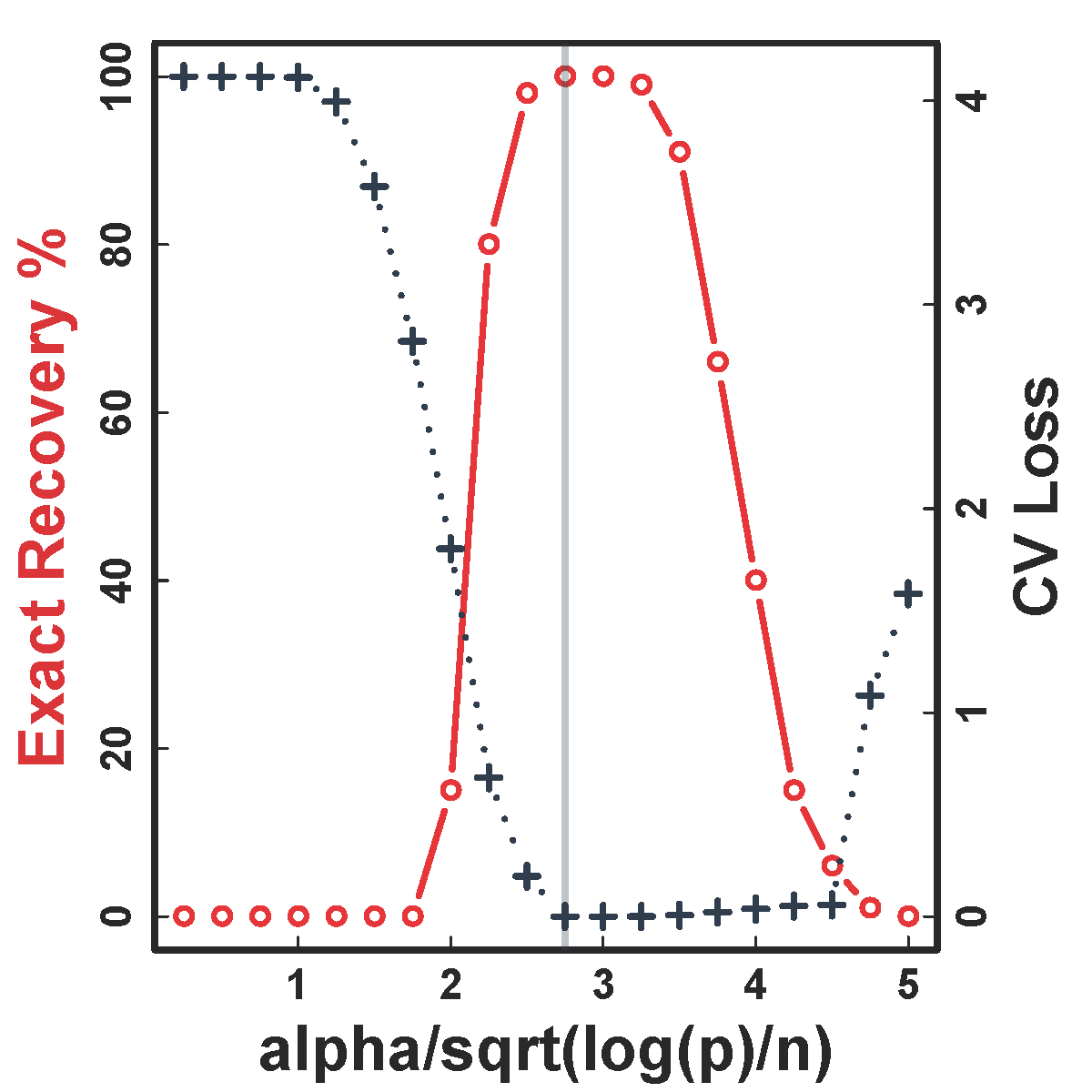

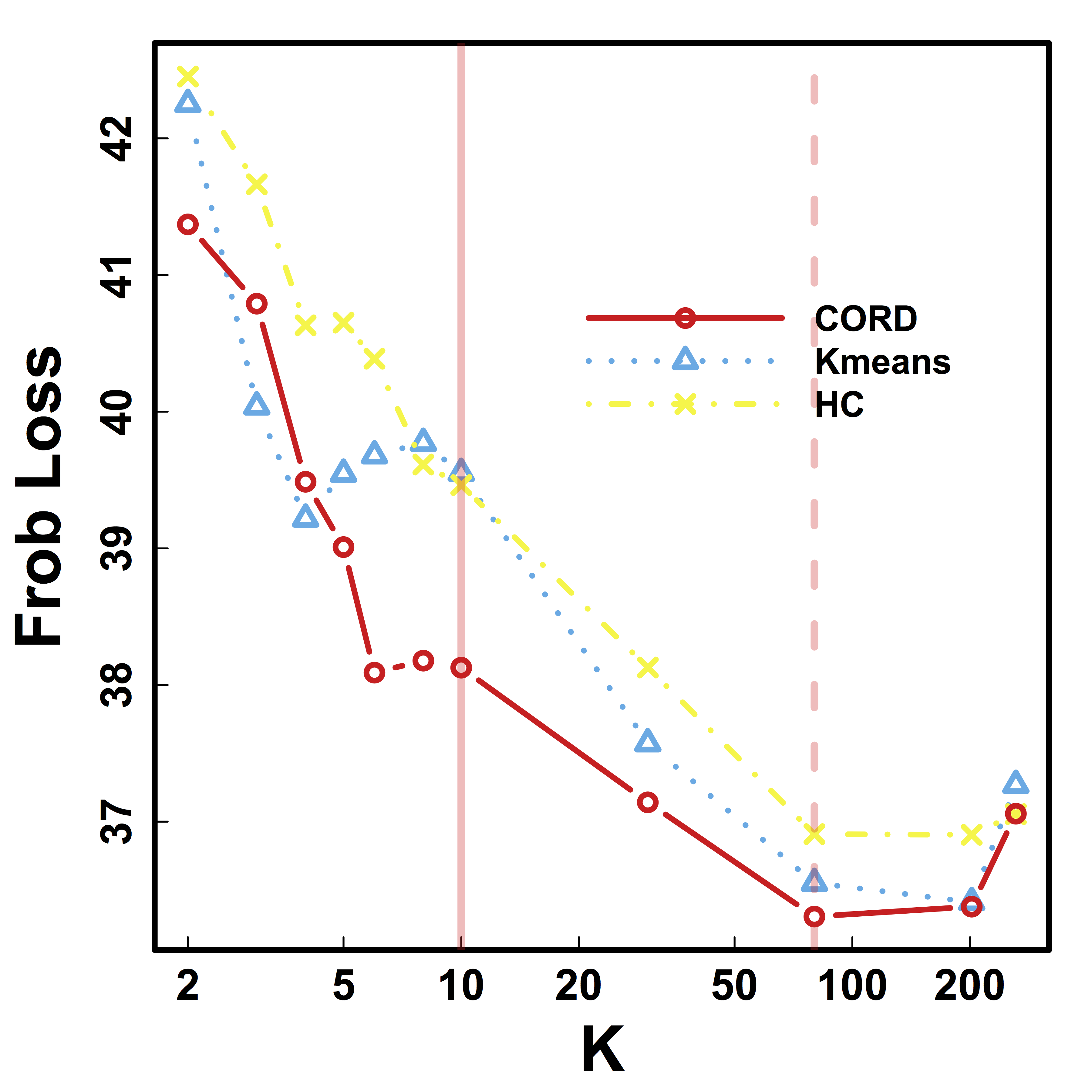

Exact Recovery

Different models for $C$="$\cov(Z)$" and $\alpha = 2 n^{-1/2} \log^{1/2} p$

Vertical lines: theoretical sample size based on our lower bound

HC and Kmeans fail even if inputting the true $K$.

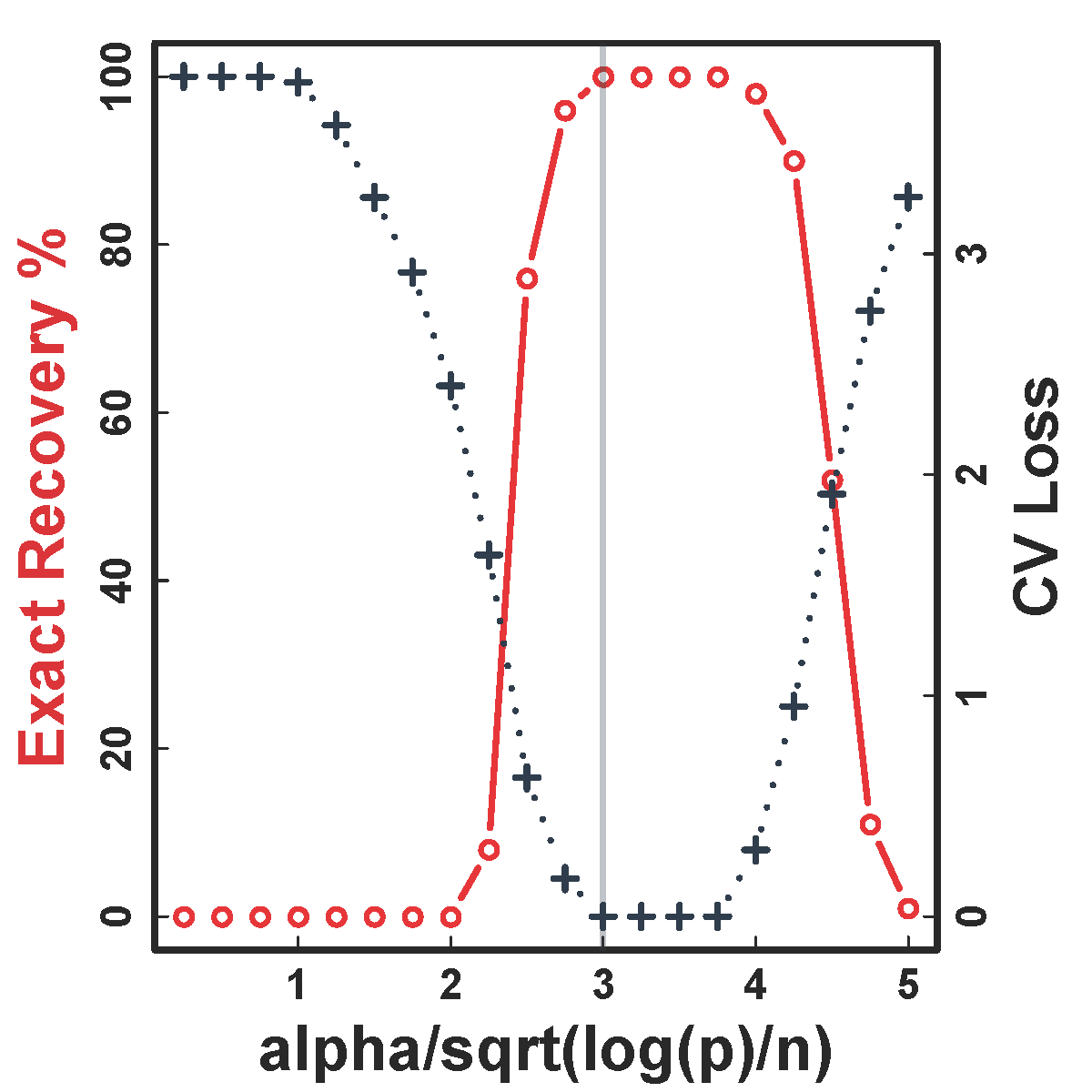

Cross Validation

CV selects the constants to yield close to 100% recovery, as predicted by our theory (at least for large $n>200$)

Real Data

fMRI Studies

Sub 1, Sess 1

Time 1

2

…

~200

⋮

Sub i, Sess j

…

⋮

Sub ~100, Sess ~4

…

This talk: one subject, two sessions (to test replicability)

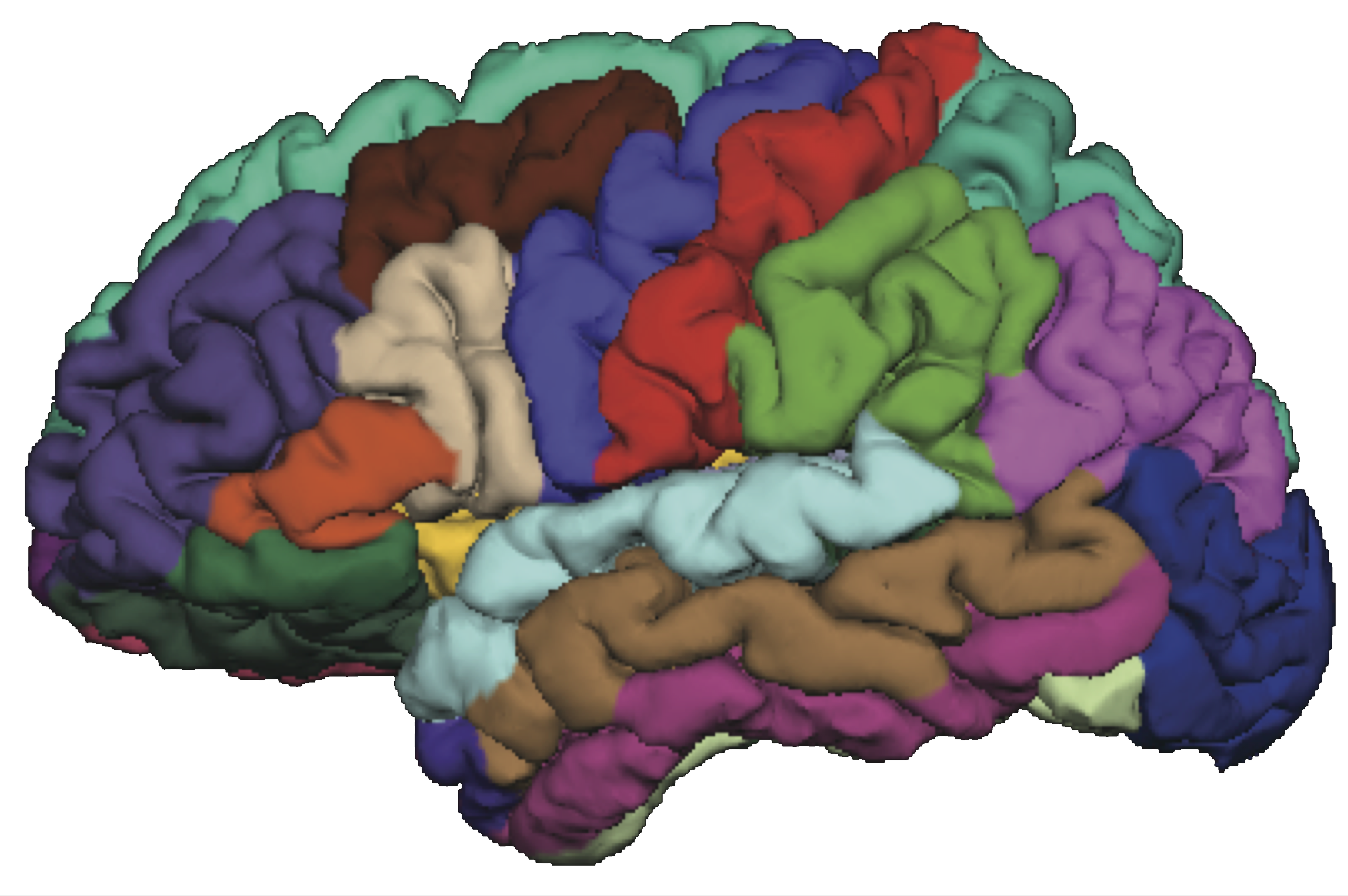

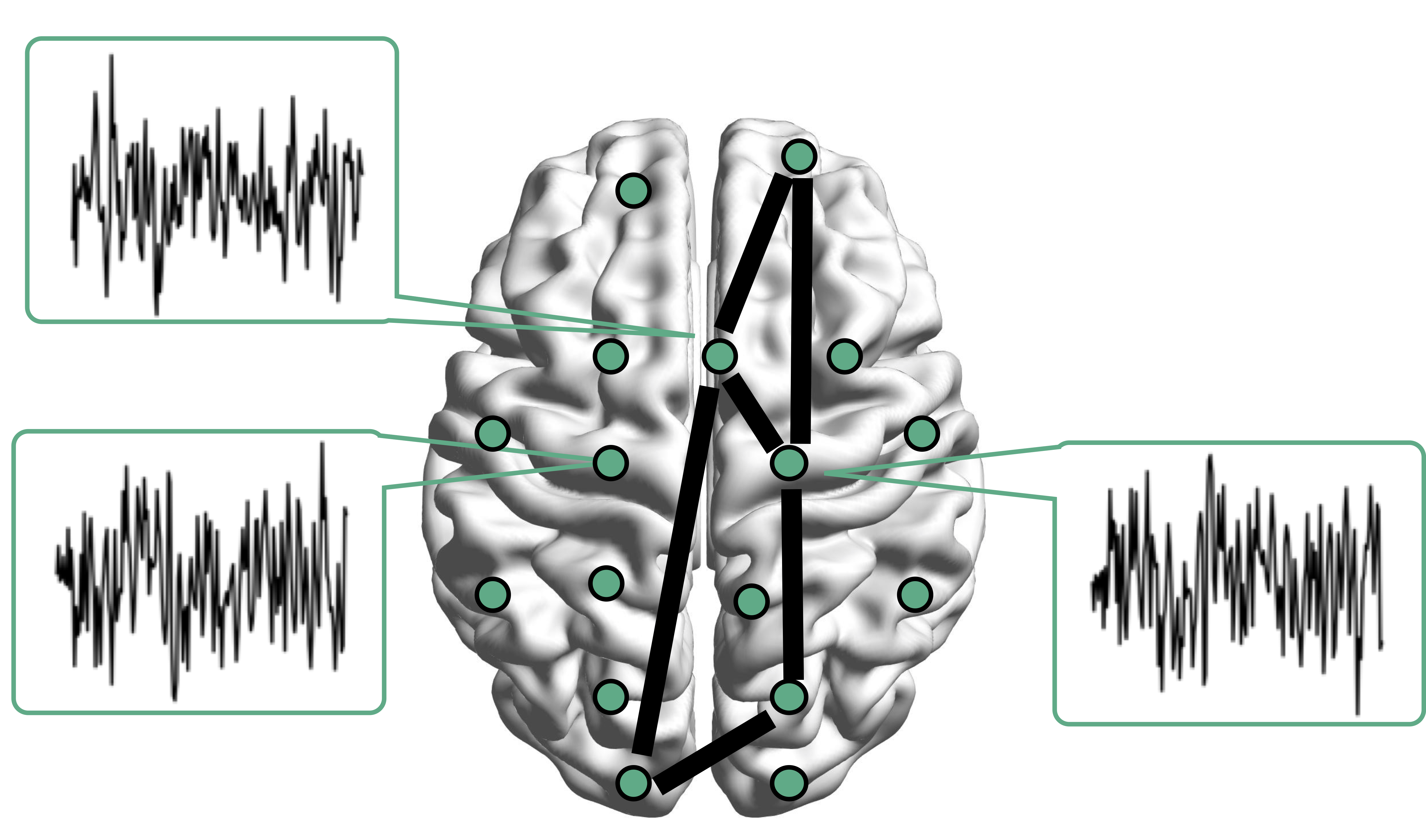

Functional MRI

- fMRI matrix: BOLD from different brain regions

- Variable: different brain regions

- Sample: time series (after whitening or removing temporal correlations)

-

Clusters of brain regions

- Two data matrices from two scan sessions OpenfMRI.org

- Use Power's 264 regions/nodes

Test Prediction/Reproducibilty

- Find partitions using the first session data

- Average each block cor to improve estimation

- Compare with the cor matrix from the second scan $$ \| Avg_{\hat{G}}(\hat{\Sigma}_1) - \hat{\Sigma}_2 \|$$ where we used $\hat{G}$ to do block-averaging.

- Difference is

smaller if clustering $\hat{G}$ isbetter

Vertical lines: fixed (solid) and data-driven (dashed) thresholds

Visual-motor task!

Discussion

- Cov + clustering = Connectivity + ROI

- Identifiability, accuracy, optimality

- $G$-models: $G$-latent, $G$-block, $G$-exchangeable

- New metric, method, and theory

- Paper: google

"cord clustering" (arXiv 1508.01939)- To appear in Annals of Statistics, 2019

- R package:

cord on CRAN

Matix Regression

Co-Authors

Yi Zhao

Johns Hopkins Biostat

Bingkai Wang

Johns Hopkins Biostat

Johns Hopkins Medicine

Brian Caffo

Johns Hopkins Biostat

Motivating Example

Brain network connections vary by covariates (e.g. age/sex)

Resting-state fMRI Networks

- fMRI measures brain activities over time

- Resting-state: "do nothing" during scanning

- Brain networks constructed using

cov/cor matrices of time series

Mathematical Problem

- Given $n$ (semi-)positive matrix outcomes, $\Sigma_i\in \real^{p\times p}$

- Given $n$ corresponding vector covariates, $x_i \in \real^{q}$

- Find function $g(\Sigma_i) = x_i \beta$, $i=1,\dotsc, n$

- In essense,

regress matrices on vectors

Some Related Problems

- Heterogeneous regression or weighted LS:

- Usually for scalar variance $\sigma_i$, find $g(\sigma_i) = f(x_i)$

- Goal: to improve efficiency, not to interpret $x_i \beta$

- Covariance models Anderson, 73; Pourahmadi, 99; Hoff, Niu, 12; Fox, Dunson, 15; Zou, 17

- Model $\Sigma_i = g(x_i)$, sometimes $n=i=1$

- Goal: better models for $\Sigma_i$

- Multi-group PCA Flury, 84, 88; Boik 02; Hoff 09; Franks, Hoff, 16

- No regression model, cannot handle vector $x_i$

- Goal: find common/uncommon parts of multiple $\Sigma_i$

- Ours: $g(\Sigma_i) = x_i \beta$, $g$ inspired by PCA

Massive Edgewise Regressions

- Intuitive method by mostly neuroscientists

- Try $g_{j,k}(\Sigma_i) = \Sigma_{i}[j,k] = x_i \beta$

- Repeat for all $(j,k) \in \{1,\dotsc, p\}^2$ pairs

- Essentially $O(p^2)$ regressions for each connection

- Limitations: multiple testing $O(p^2)$, failure to accout for dependencies between regressions

Model and Method

Model

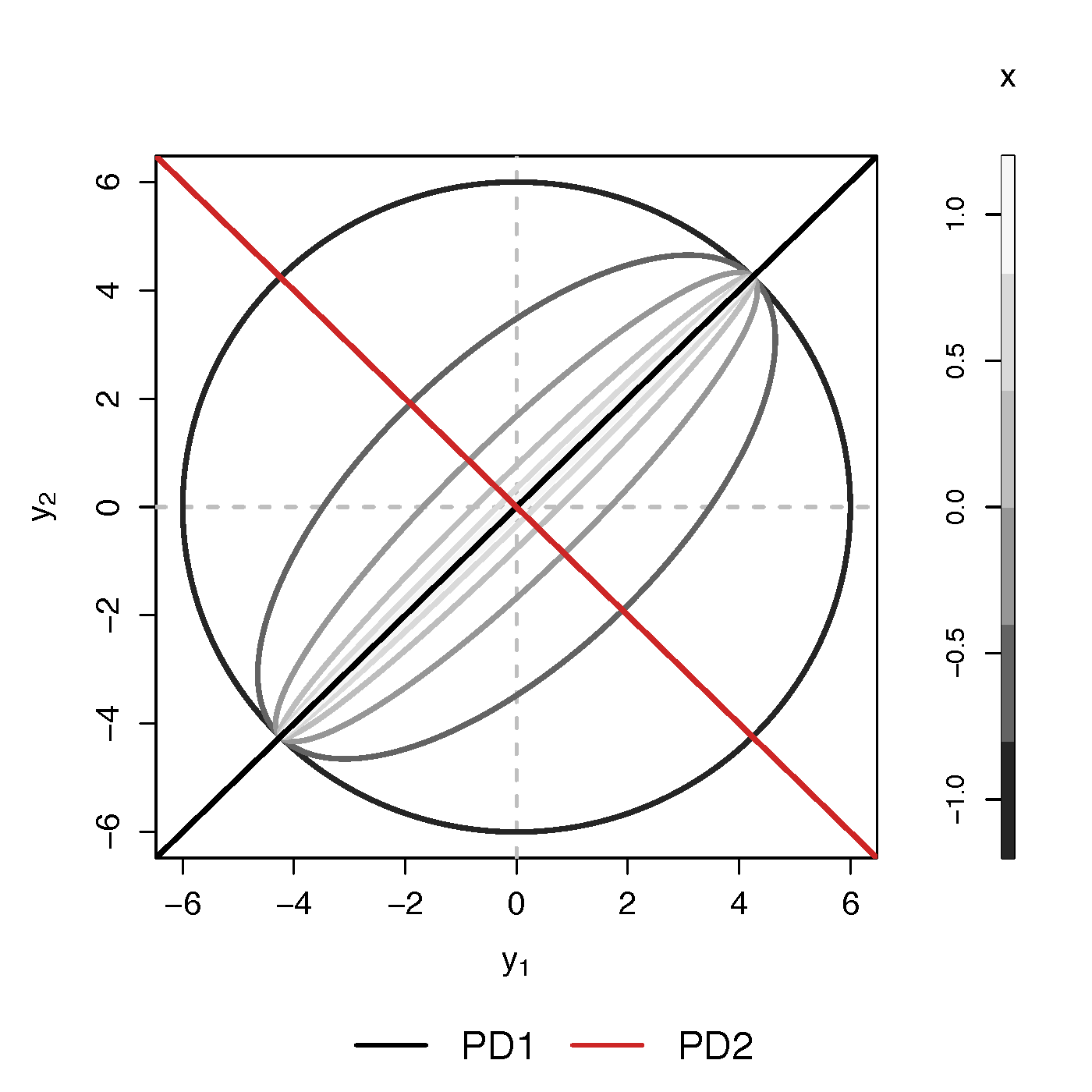

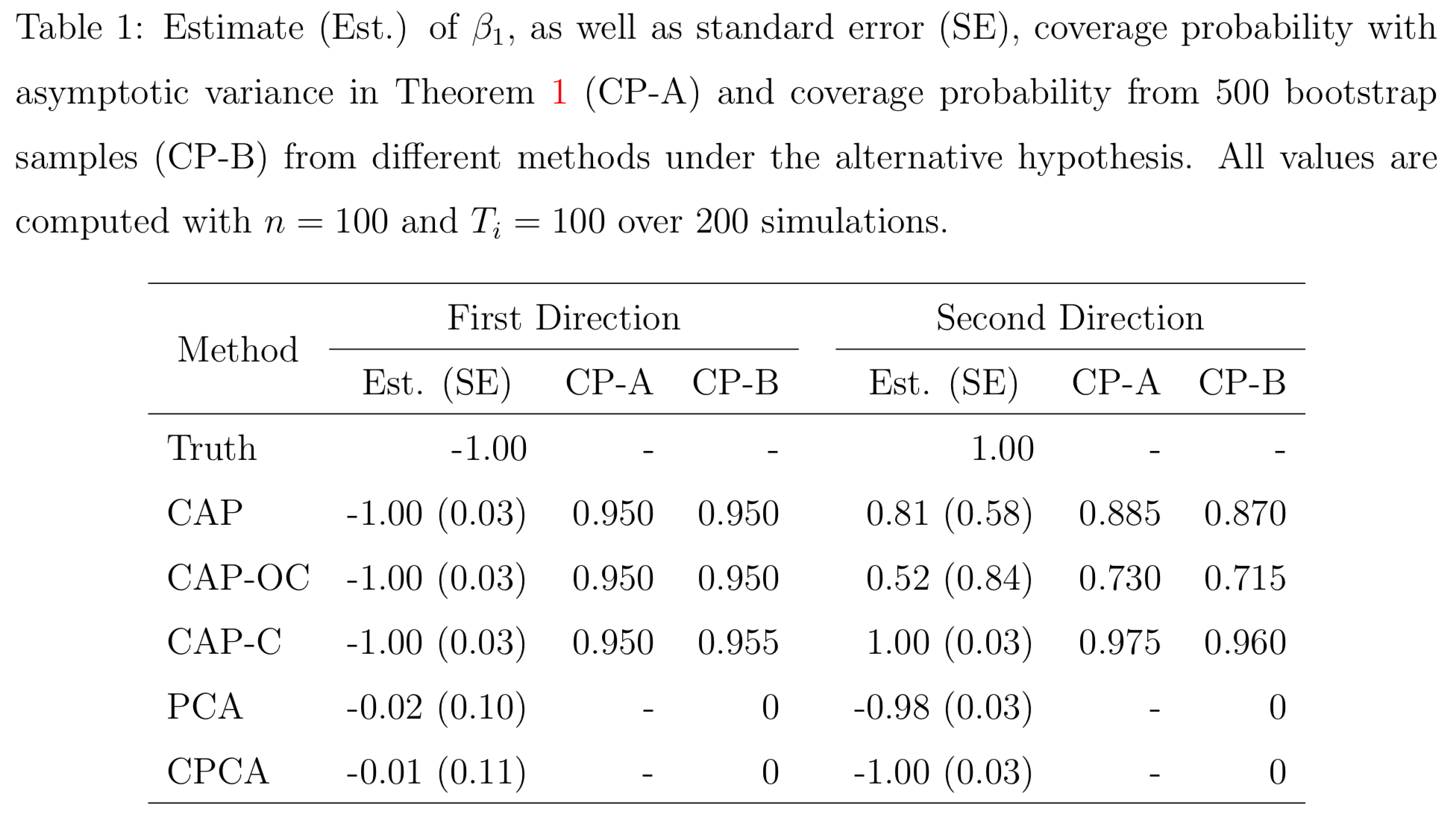

- Find principal direction (PD) $\gamma \in \real^p$, such that: $$ \log({\gamma}^\top\Sigma_{i}{\gamma})=\beta_{0}+x_{i}^\top{\beta}_{1}, \quad i =1,\dotsc, n$$

Example (p=2): PD1 largest variation but not related to $x$

PCA selects PD1, Ours selects

Advantages

- Scalability: potentially for $p \sim 10^6$ or larger

- Interpretation: covariate assisted PCA

- Turn

unsupervised PCA intosupervised

- Turn

- Sensitivity: target those covariate-related variations

Covariate assisted SVD?

- Applicability: other big data problems besides fMRI

Method

- MLE with constraints: $$\scriptsize \begin{eqnarray}\label{eq:obj_func} \underset{\boldsymbol{\beta},\boldsymbol{\gamma}}{\text{minimize}} && \ell(\boldsymbol{\beta},\boldsymbol{\gamma}) := \frac{1}{2}\sum_{i=1}^{n}(x_{i}^\top\boldsymbol{\beta}) \cdot T_{i} +\frac{1}{2}\sum_{i=1}^{n}\boldsymbol{\gamma}^\top \Sigma_{i}\boldsymbol{\gamma} \cdot \exp(-x_{i}^\top\boldsymbol{\beta}) , \nonumber \\ \text{such that} && \boldsymbol{\gamma}^\top H \boldsymbol{\gamma}=1 \end{eqnarray}$$

- Two obvious constriants:

- C1: $H = I$

- C2: $H = n^{-1} (\Sigma_1 + \cdots + \Sigma_n) $

Choice of $H$

Will focus on the constraint (C2)

Algoirthm

- Iteratively update $\beta$ and then $\gamma$

- Prove explicit updates

- Extension to multiple $\gamma$:

- After finding $\gamma^{(1)}$, we will update $\Sigma_i$ by removing its effect

- Search for the next PD $\gamma^{(k)}$, $k=2, \dotsc$

- Impose the orthogonal constraints such that $\gamma^{k}$ is orthogonal to all $\gamma^{(t)}$ for $t\lt k$

Theory for $\beta$

Theory for $\gamma$

Simulations

PCA and common PCA do not find the first principal direction, because they don't model covariates

Resting-state fMRI

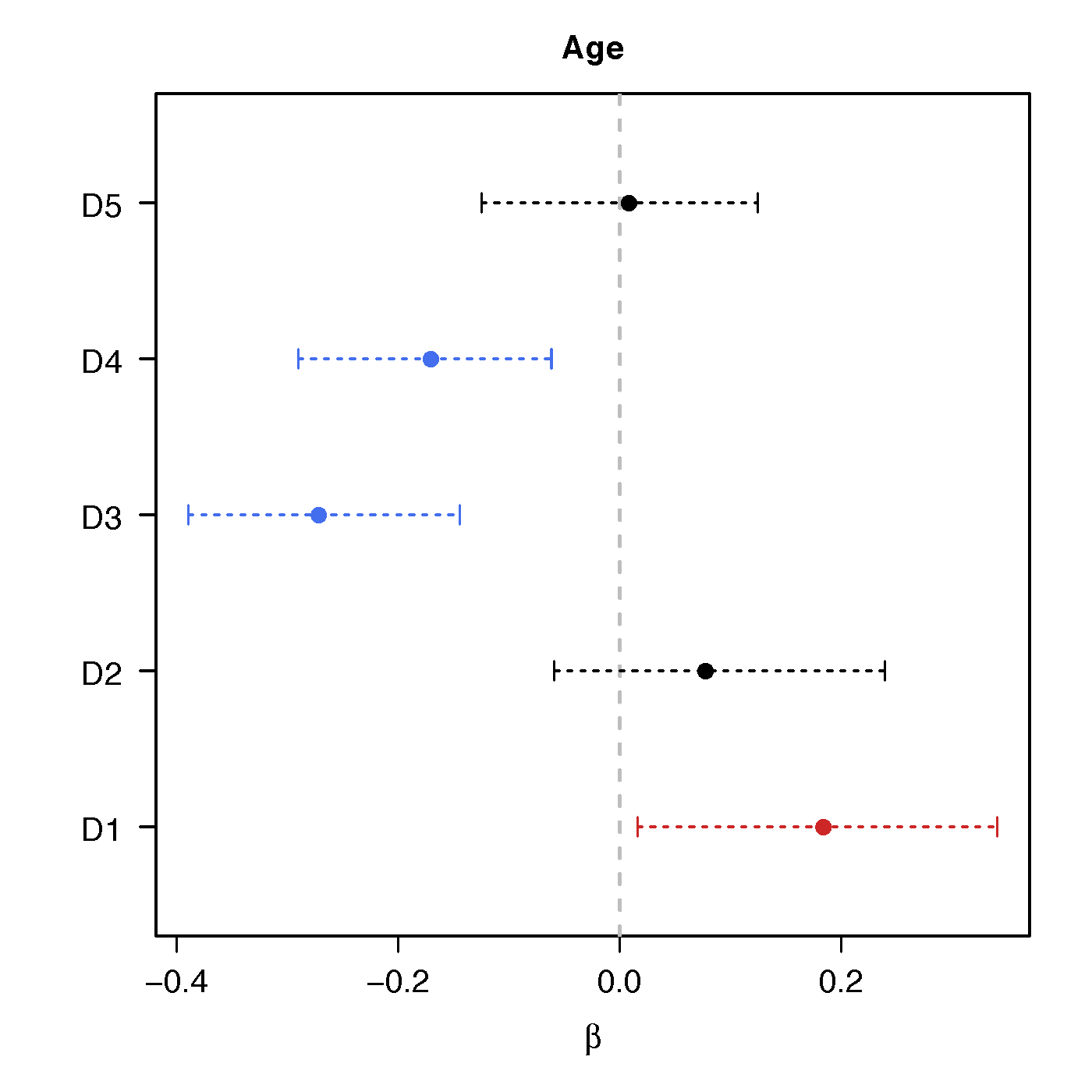

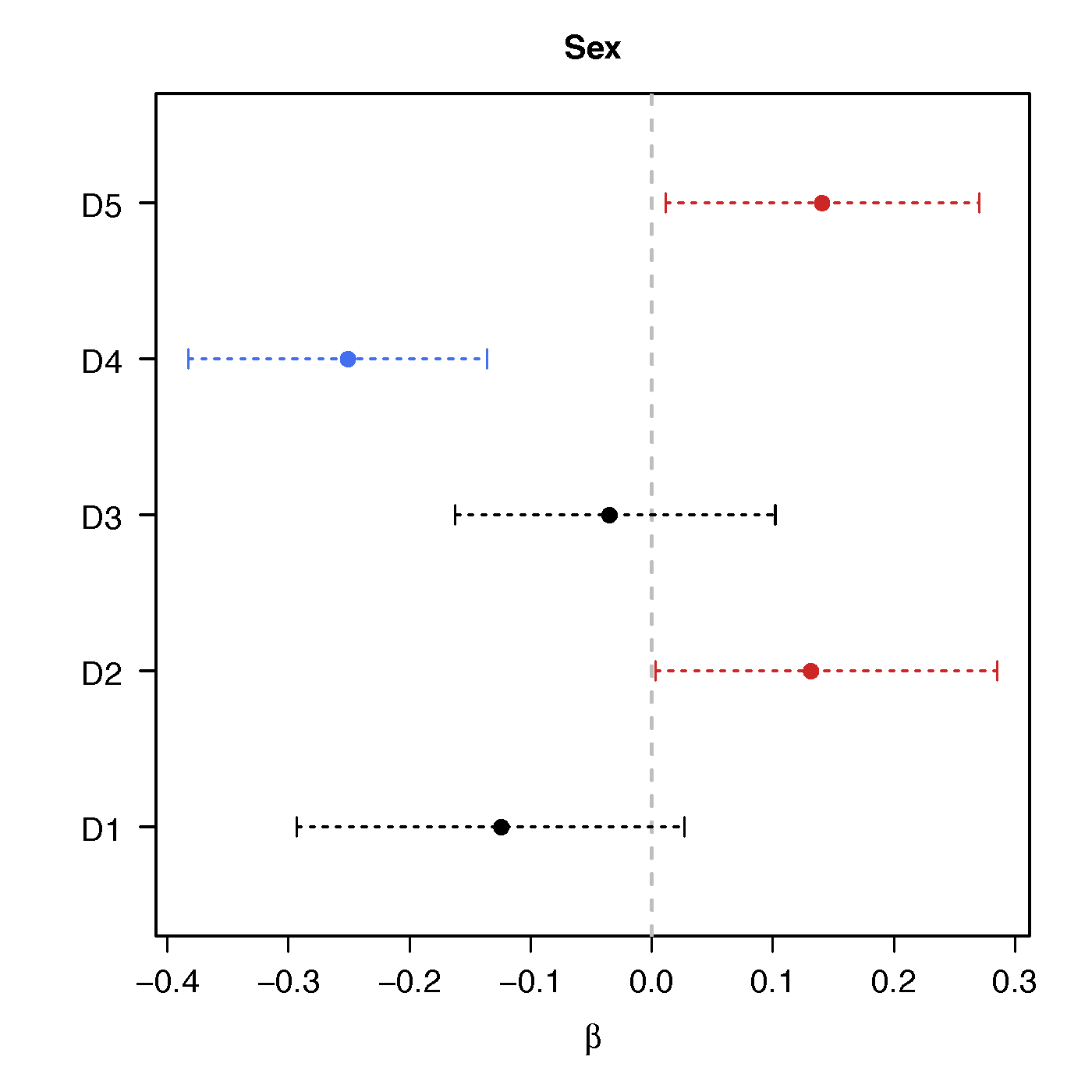

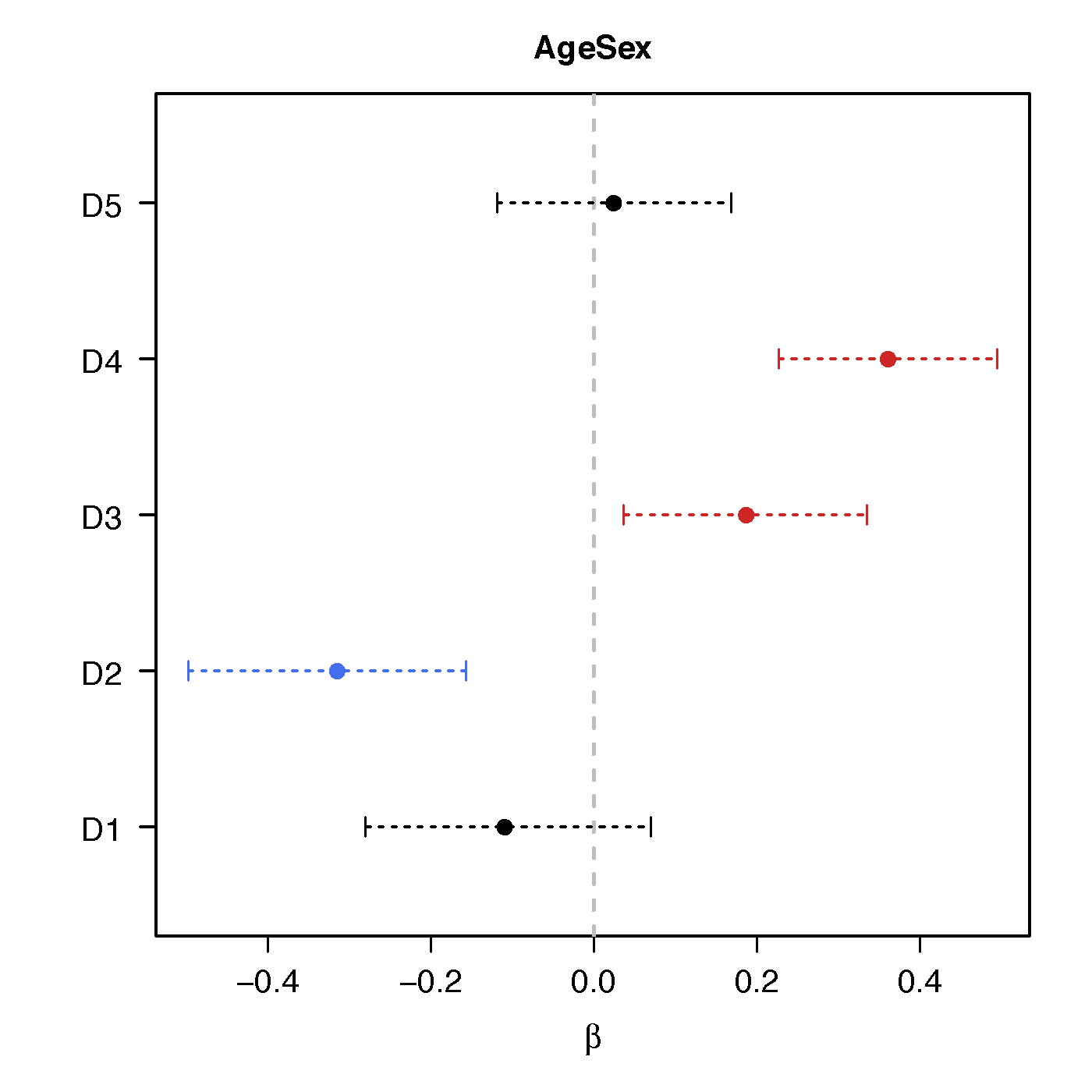

Regression Coefficients

Age

Sex

Age*Sex

No statistical significant changes were found by massive edgewise regression

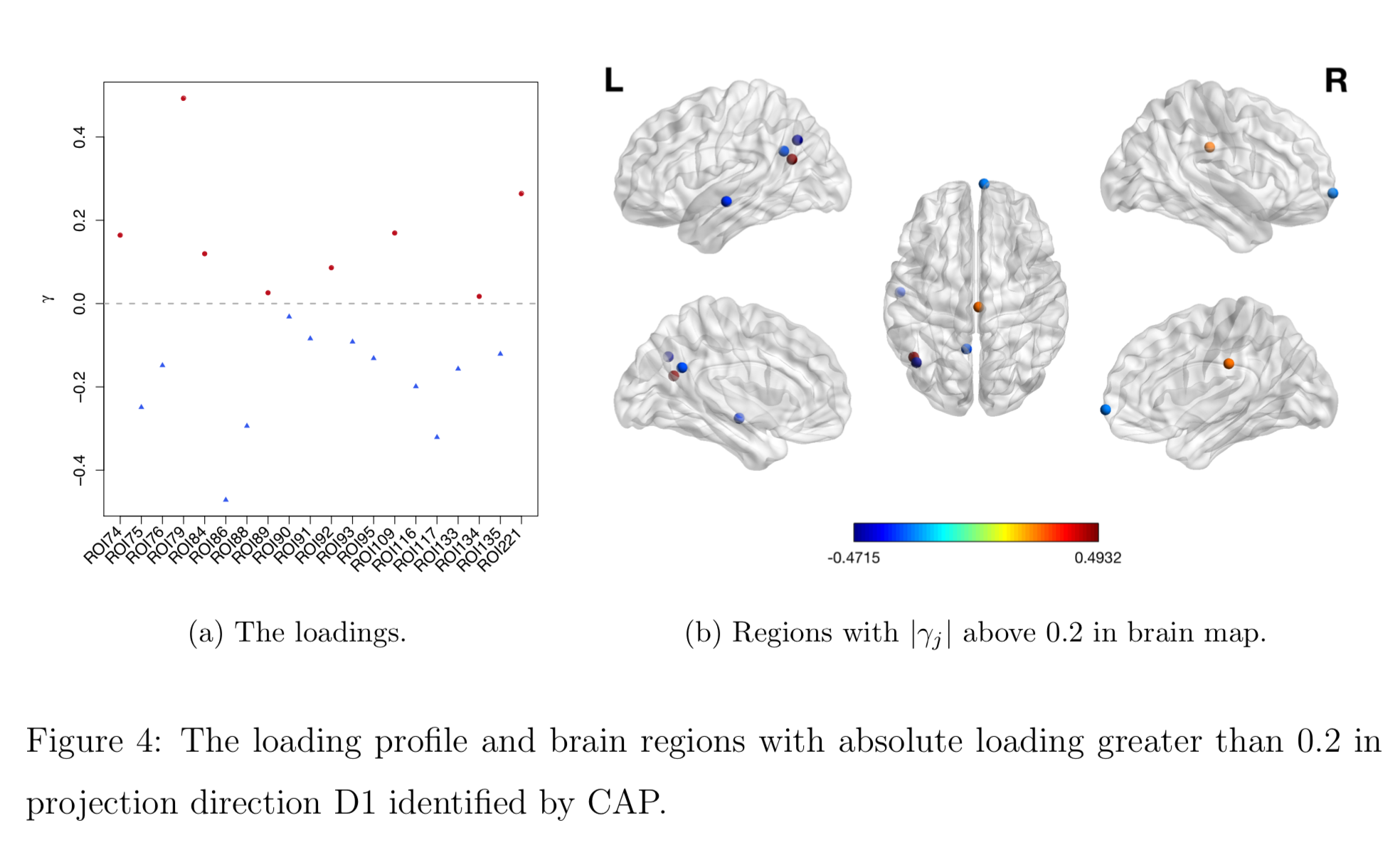

Brain Map of $\gamma$

Discussion

- Regress matrices on vectors

- Method to identify covariate-related directions

- Theorectical justification

- Manuscript: DOI: 10.1101/425033

- R pkg:

cap